You might have heard about how bank costs increase as the bank crosses the infamous mark of $10 billion in assets.

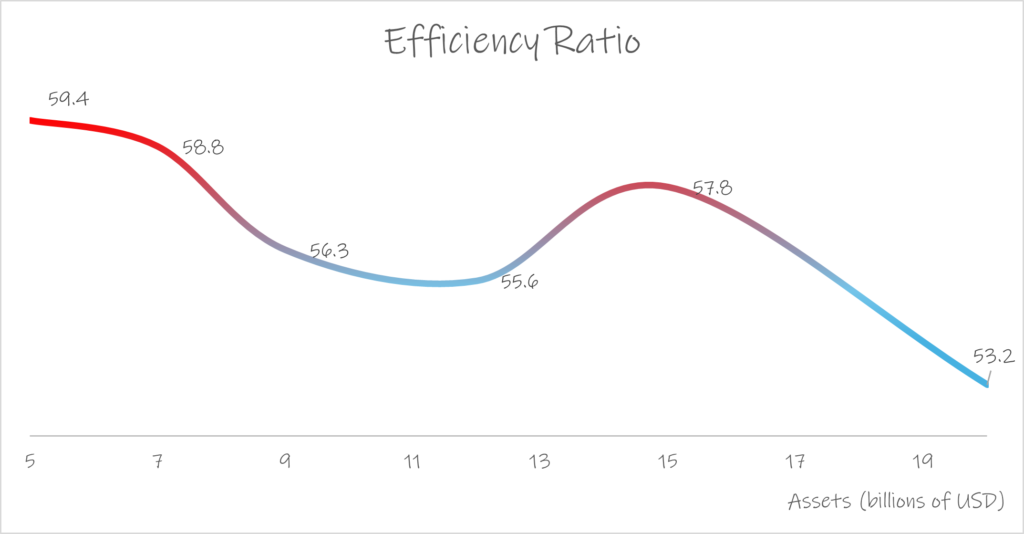

This is the average efficiency ratio for all US banks by size for 2019 through 2023.

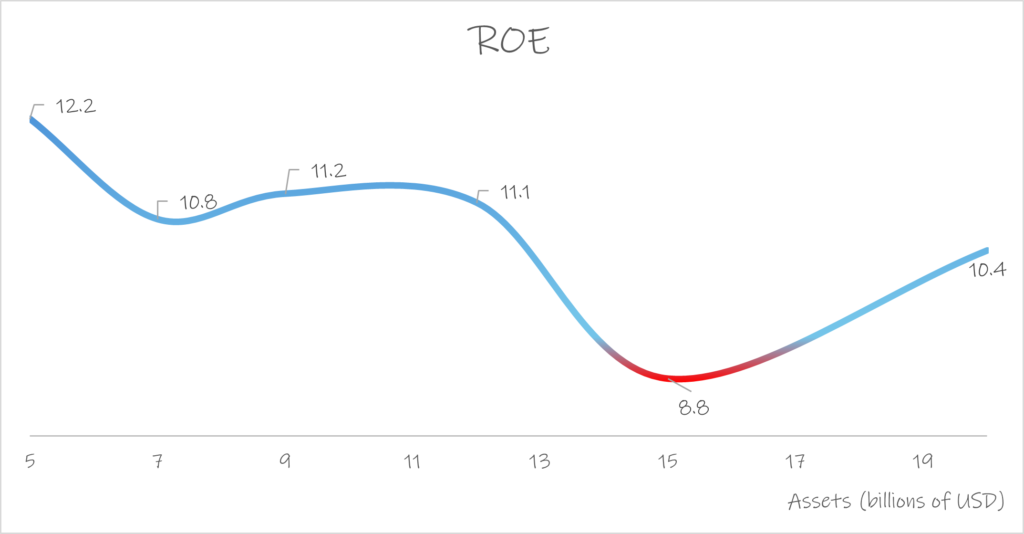

And this was their average ROE:

As you can see, as banks grow, they benefit from economies of scale, which is reflected in their efficiency ratio and profitability. This seems particularly potent after the bank crosses the $7 billion mark. Then, the trend takes a turn for the worse, wiping out all gains as the bank approaches $15 billion before it resumes its downward march.

The main message: prioritize growth

For community banks of all sizes, preparing your strategy with this curve in mind is extremely important. Many banks see profitability and efficiency as their single top priority and fail to see that many of their margin problems require growth to be solved.

For example, several system integrations that drive efficiency are not viable until the bank has reached a minimum size. The same is true for customer acquisition and relationship nurturing – both critical drivers of margins and profitability.

Prepare for growth

It may be tempting to acquire your way out of the “slump”. Buying 2-3 smaller banks has the potential to accelerate your $10-20 billion transition from 10 to 20 years to 5 to 10 years.

Banks who want to “speed up through the slump” effectively need to start preparing years before they execute it. Among other things, they need to answer six strategic questions:

- Can we use smaller, low-stakes acquisitions to “learn the ropes”?

If they are an option, small acquisitions can help you learn how to identify, negotiate, acquire, and integrate other banks into your organization. Making your first acquisition when your strategy is on the line often turns you into another statistic of why acquisitions fail. - What preparations do we need to make to our balance sheet and funding?

This is particularly relevant if your shareholders do not want to be diluted, but valid even if that is not the case. Your bank will require significant new investment in compliance, technology and infrastructure, and lack of foresight can leave you stranded and unable to deliver on your M&A plan. - What should be our acquisition model?

Considering your strategy and potential targets in your markets, should you aim at one big merger or several small acquisitions? Should you look for targets in your markets or targets with the potential to help you in areas you are sub-scale? Do you plan to continue growth inorganically and need to create a production line, or is this just a temporary thing? - How can we avoid a “chicken flight”?

Even though compliance requirements change when banks cross the $10 billion mark, this does not immediately translate into incremental costs. As the chart shows, most banks start realizing all the implications (and costs) of their new reality by the time they get to $11 or $12 billion. Preparing for a marathon, not a sprint, is vital to avoid losing traction as other areas start demanding your attention. - What business portfolio will give me the best scaling capabilities? Not all businesses and combinations of businesses are equally easier to scale up. And, as banks grow, complexity (especially as compliance requirements increase) can be a drag on your scarce resources. Pre-emptively choosing the right business portfolio can significantly improve your future scalability. By the same token, deciding and focusing your innovation portfolio in areas that will help you scale up pays handsome dividends.

- How can we make it easier for new customers? Acquiring new customers is often an essential part of a growth strategy. However, many banks that compete on “personable services” and “strong relationships” optimize their experience for their existing customers. For example, risk policies and underwriting processes often allow for exceptions to accommodate the needs of good (i.e. existing) customers.

Conclusion

Bank economics change significantly as you grow and a good strategy needs to consider that. And because some decisions like using “learning acquisitions”, preparing your balance sheet, settling on an acquisition model, securing long-term reserves, and fine tunning your business portfolio and new customer journey can take years to materialize, banks should start this journey several years before they are necessary.

Let us help you achieve greater and more profitable growth HERE.