Let us help you achieve greater and more profitable growth. Click here.

As you probably know, worldwide, Open Banking is one of the hottest trends in financial services.

Not only is it growing at a breakneck speed, but also its success is inspiring regulators and players in other sectors like finance and insurance who now wonder how to replicate the model.

This article is a high-level review of what is happening in Open Banking today.

Growth

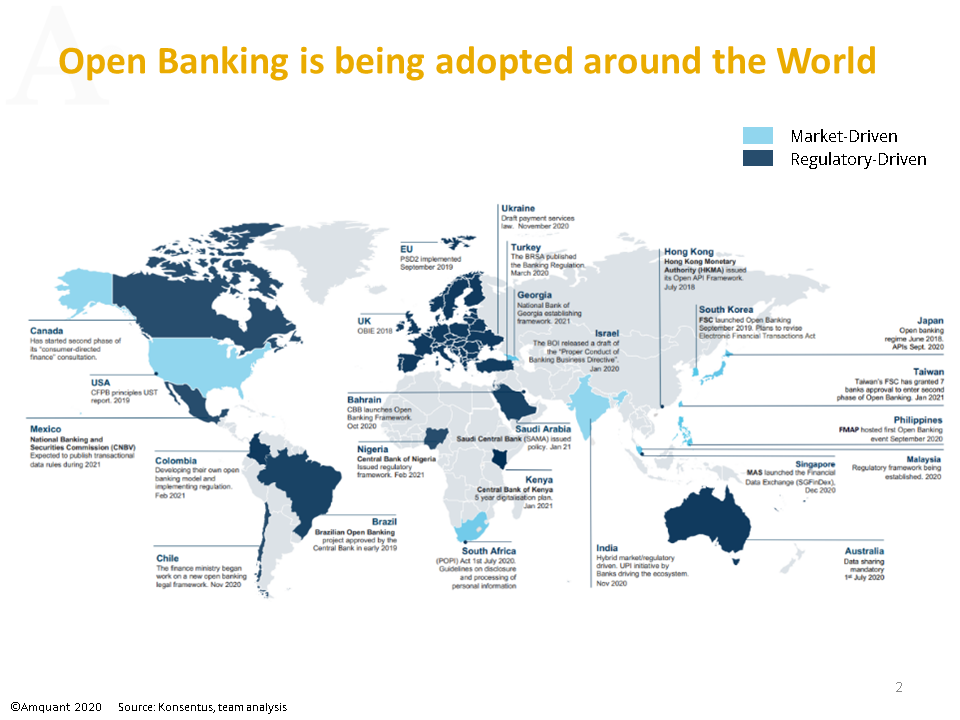

As I said, Open Banking is growing. To understand how fast it grows, consider that the UK (the pioneer in adopting it) formally started this journey less than three years ago, followed by Hong Kong, the EU, South Korea and Singapore. In the US, the Consumer Financial Protection Bureau joined the race in 2019. Twenty other countries followed suit, including Canada, Australia, India, Japan, Israel and India.

As a result, high growth rates in each market are being compounded by the entry of new markets.

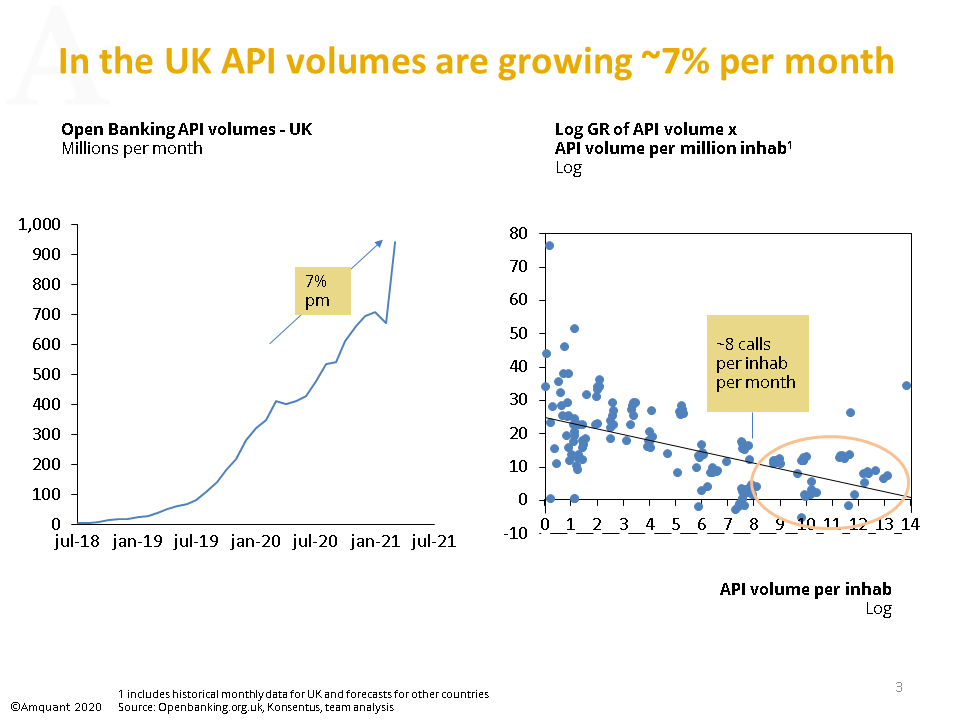

For example, in Europe, when a market opens, it has explosive growth, which tends to stabilize in the single digits range (per month) once it reaches ~8 API calls per inhabitants per month. But, as the UK “stabilizes”, new entrants like Italy, Germany and France push the averages up.

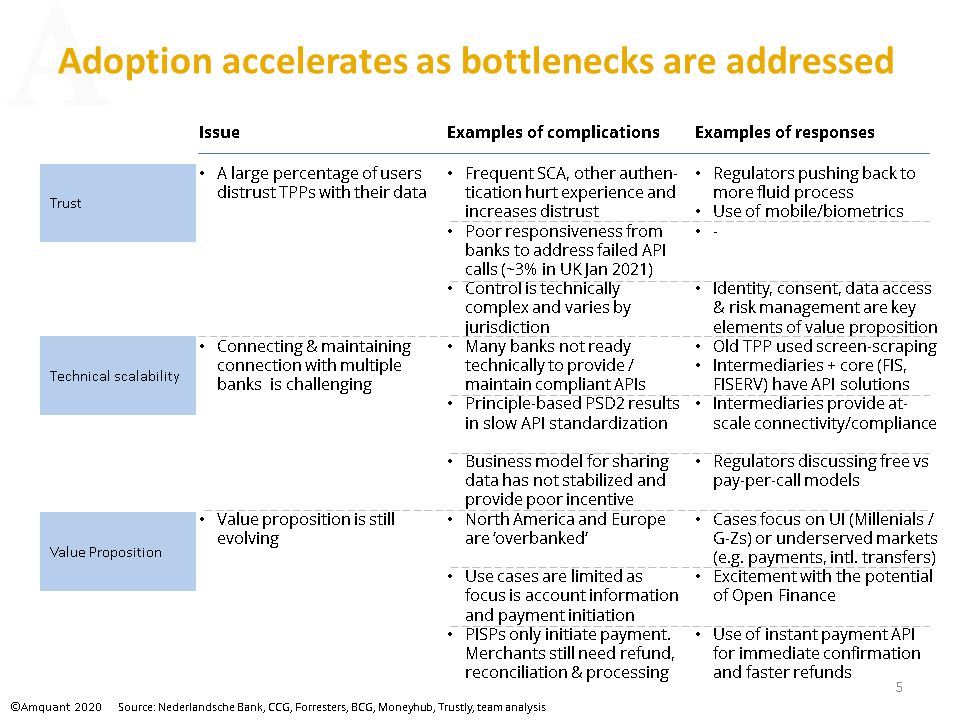

Debottlenecking

Three types of factors “repress” the adoption of Open Banking-based services:

- Lack of trust: the fact that many users distrust TPPs with their data,

- Technical scalability issues: the fact that connecting and maintaining connections with multiple banks is challenging, and

- Poor value proposition: the fact that the value proposition is still evolving.

Each of these factors is not a “single” issue but many context-specific bottlenecks, each requiring several solutions. As players find and implement these solutions, adoption grows.

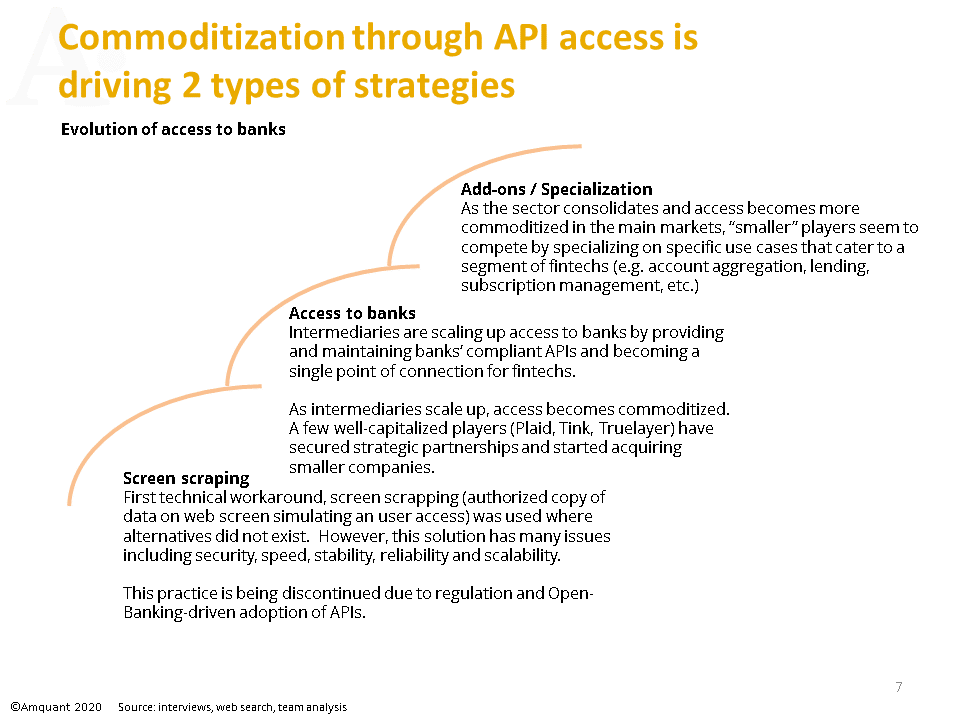

So, for example, one initial “solution” to technical scalability issues was the use of screen scraping solutions by Fintechs (authorized by the user, the Fintech accesses the user’s account with a financial institution and use the information on screen to source its data). Screen scraping fueled adoption, but it has many obvious issues (speed, security, scalability, among others) – so as API-based solutions grow, a new wave of service adoption is fueled.

Intermediaries

Intermediaries emerge in this space, providing a single point of connection to TPPs and an easy-to-maintain compliant API solution for banks.

For example, fintechs do not need to connect with every bank in its market and maintain these connections, each evolving differently. They connect with one provider. On the flip side, banks use these intermediaries to provide, maintain and manage compliant APIs.

Intermediaries are already consolidating and fighting the commoditization of these services by forking into two distinct strategies:

- One based on scale and simple universal access to financial institutions – adopted by a few well-capitalized companies with access to a large number of banks and strategic partners (e.g. Plaid/VISA, Tink/Paypal) and

- One based on scope and value-added/use-case specialization – adopted by the vast majority of companies in this space.